Treasury yield curve un-inversion fears inflation, supply tsunami, hits QT milestone. Mortgage rates are around 7%

The 10-year yield rose 60 basis points in five weeks but may be running out of steam now.

By Wolf Richter for WOLF STREET.

The 10-year Treasury yield rose to 4.25% on Friday, up 60 basis points from the day before the Fed's monster rate cut (when the 10-year yield was 3.65%), and up 5 basis points from a week ago. This 4.25% is a milestone of sorts.

The 10-year yield has now reached its highest level since July 25. What a three-month round trip! On July 25, long-term yields began to accelerate their decline as Fed rate cut bets gained momentum on sub-par labor market data and cooling inflation, and continued to decline until the Fed actually cut 50 basis points. On September 18, to the surprise of many, especially in the home sales industry, long-term yields moved higher rather than dropping further.

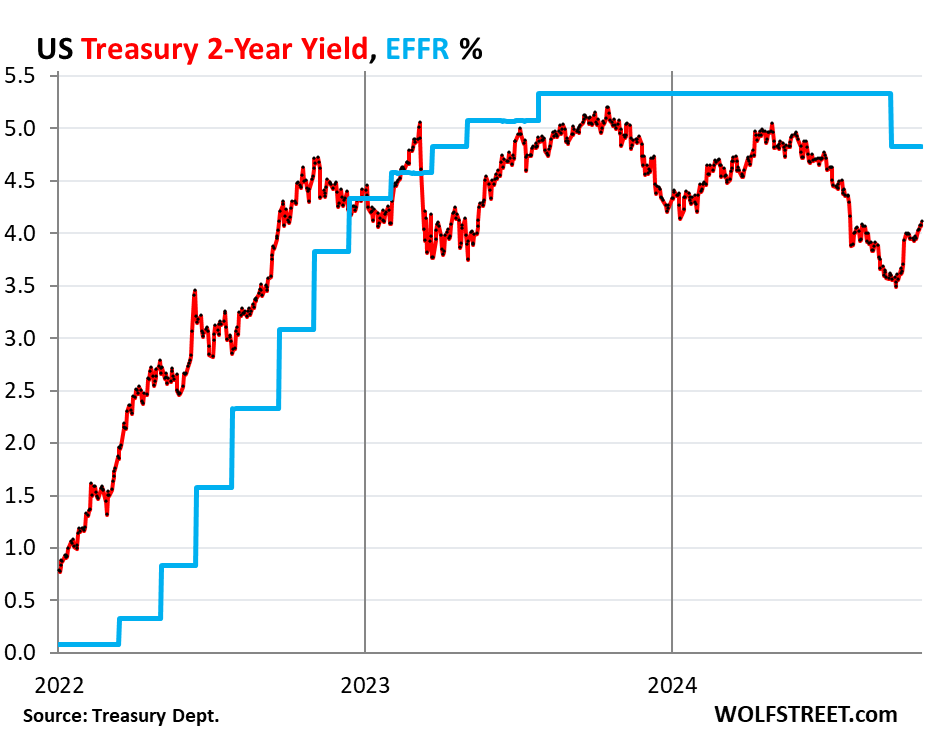

And about two weeks after the rate cut, a series of big everything-up revisions began to follow, one after the other, a strong labor market and higher and rising inflation. And yields rise (blue = the effective federal funds rate that the Fed targets with its headline policy rate):

But short-term yields have continued to decline, pricing in at least one 25-basis point cut this year, but are skeptical of a second 25-basis point cut. Mega-cut off the table. And they're pricing in cuts next year, but more slowly than a few months ago.

“Yield Curve” The process of un-reversal continues between a simultaneous increase in long-term yields and a decrease in short-term yields.

The normal state of treasury yields is that long-term yields are higher than short-term yields. The yield curve is considered “inverted” when long-term yields are below short-term yields, which began to occur in July 2022 as the Fed quickly raised policy rates, pushing up short-term Treasury yields, while long-term yields also rose but more slowly. The yield curve is now in the process of normalization.

The chart below shows the “yield curve” with Treasury yields across the spectrum of maturities from 1 month to 30 years on three key dates:

- Gold: July 25, 2024, before labor market data goes into tailspin.

- Blue: September 17, 2024, the day before the Fed's mega-rate cut.

- Red: Friday, October 25, 2024.

The 7-year maturity yield is now (red) about where it was on July 25 (gold). This is the milestone.

And notice how far those yields have risen since the day before the rate cut (blue line). Everything from 3-year to 20-year yields rose 60 basis points or more. It was a big quick round trip, going down in two months, back the same distance in one month, amid a lot of volatility in the Treasury market.

Two-year Treasury yield It was above 4% all week and closed Friday at 4.11%, the highest since August 1. This has partly come about because aggressive rate-cut expectations have returned after a series of all-up revisions.

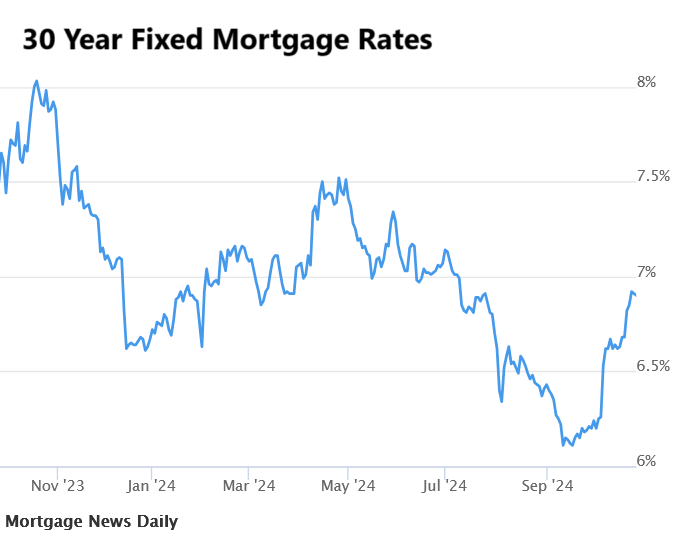

mortgage ratesThat's roughly parallel to the 10-year yield but higher, up from the low-point just before the rate cut. The Mortgage News Daily's daily measure for the 30-year fixed-rate mortgage is now 6.90%, from a low of 6.11% on the eve of the rate cut in a little more than a month.

Mortgage rates were typically above 6% in the decades before QE, and for long periods above 7% to 8%, and there were years of much higher rates (chart via Mortgage News Daily).

For the real estate industryThis turn of events was very unexpected. They promised buyers and sellers that mortgage rates, which had already fallen from about 8% a year ago to about 6% in mid-September, even on a wing-and-pray basis, without a rate cut, would continue to plunge, and 4%. There was talk of loss or whatever.

Despite the plunge in mortgage rates from the end of October to 17 September 2023, sales of existing homes have fallen – because prices are too high. And in the past few weeks, sales volumes have worsened, as we can see from the drop in mortgage applications.

The problem with the housing market today – with sales of existing homes on track to plunge to the lowest volume since 1995 in 2024 – is not mortgage rates; They are back to normal. The free-money era of the pandemic has seen house prices explode by 50% or more in many markets in less than three years, in many cases topping already precariously high values.

These prices are too high, they are not economically feasible, they are not understandable Seeing this, many buyers went on strike. But mortgage rates are now back in the normal range.

The drivers…

Longer-term yields, particularly 10 years and beyond, are driven by inflationary assumptions over the life of the security and the assumption of a supply of new Treasury securities to finance huge deficits.

Fear of inflation Great motivator. No investor wants to hold a Treasury security with 10 years remaining, and with a purchased yield of 3.6%, when the average inflation rate over the life of the security is 4% or 5% or 6%.

A Tsunami of New Treasury Securities Supply Currently, deficit financing is washing the ground every week, and Congress and those in the White House seem unwilling to have a serious conversation with the American people about it. So debt has ballooned, and bond investors see no relief on the horizon.

Fed's QTA third factor drives long-term yields to some extent. The Fed switched to QT in 2022, after trillions of dollars of reckless QI, which depressed long-term yields and mortgage rates to record lows and caused all sorts of mega-problems, including crazy spikes in house prices. So far, the Fed has shed nearly $2 trillion from its balance sheet. And the QT rate continues despite the reduction.

How much further can the 10-year yield go?

The 10-year yield is up a lot, and fast, and our gut feeling is that it's about to run out of steam.

If the next few inflation readings are benign, and labor market data weakens again, in such a scenario, the 10-year yield will likely close.

But core CPI inflation accelerated on a month-to-month basis for the third month in a row, and if it remains higher for the next several months, driven by continued strong demand and a tight labor market, the 10-year yield could try to climb a few more steps. That would push mortgage rates back over 7%.

Enjoy reading Wolf Street and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to learn how:

Would you like to be notified by email when WOLF STREET publishes a new article? Sign up here.

![]()